Written by: Pierre Maartens | Farm Business Consultant | 0457 162 484

The reality that we live in a globally connected world was once again confirmed to me after spending a few weeks in South Africa, where my family operate a sheep farm. The domestic challenges are different and unique, but farmers are facing the same challenge with lower sheep prices.

Key Points:

- Global sheep supply numbers are high.

- Global demand is a constraint – effects of high inflation/ cost of living pressures.

- Local supply is positive after a few good seasons.

- Local demand is stable/subdued – inflation/cost of living pressures.

- Medium/Long term outlook is positive.

Compounding interest is sometimes called the eighth wonder of the world and I think the law of supply and demand is the ninth wonder, which defines the relationship between the price of a product and the people’s willingness to either buy or sell it. The concept was made famous by Adam Smith in 1776.

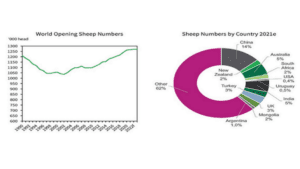

From a global perspective, sheep numbers lifted to record levels of 1.266 billion in 2021, the growth in sheep numbers for the past decade was in response to high prices and demand for sheep meat. China, India and Australia have the largest sheep populations. The significance of Australia as a major player can be underestimated by the fact that Australia has 5% of the sheep population, but it is the largest exporter of sheep meat in the world and is the top wool production nation with 18% of world production. It is clear from above that Australia is an exporting nation and that our sheep population is underpinned by the merino. The future is positive with our biggest competitor in the sheep meat market New Zealand having reduced its flock from around 48.8M in 1995 to 25.8M in 2021.

Source: OECD Agricultural Outlook

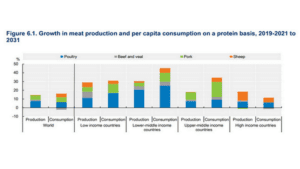

Being an exporting nation it is important to understand our key/growth markets. Growth in global consumption of meat proteins over the next decade is projected to increase by 14% by 2030. Sheep meat is expected to increase by 16% by 2030 (as per the graph below). We are seeing an increase towards poultry, whilst in high-income countries we have seen a more stable market with a shift towards white meat and consumers concerned about health, animal welfare and the environment. In Australia plant-based protein accounts for 0.6% of fresh meat volume sales.

Source: OECD Agricultural Outlook

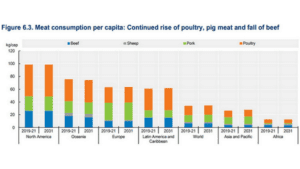

Economic growth is an important driver of meat consumption but is complex. Low-income countries – where a large % of income is spent on food, people spent a greater % on lower-valued foods such as carbohydrates.

The main opportunity for Australia is in the lower middle and upper middle countries where we have seen an increase in GDP which results in a change in meat consumption.

On a global scale sheep meat is niche product with global consumption at 1.8kg/year, whilst the Australian average is 5.9kg/year, compared to beef with global consumption at 5.4kg/year, whilst the Australian average is 19.2kg/year.

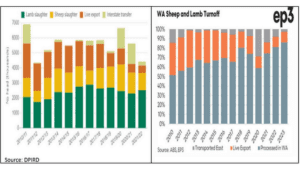

What about the numbers in WA, the state flock is around 12.5M or 19% of the national flock. It is important to understand these turnoff numbers as they present the demand side of the sheep price equation.

Turnoff in 2021 consists of domestic slaughter at 75%, with 19% domestic consumption and 81% exported, live export at 11% and interstate transfers at 14%, during 2022 and 2023 interstate transfers have reduced due to improved seasonal conditions in the Eastern States, live export numbers have been stable/reducing, which has put more pressure on local processors who have experienced labour and logistics challenges. These are the reasons behind the current lower sheep prices.

What about the remainder of 2023 and beyond?

No major changes can be made to your sheep enterprise now, the time has passed for that. But do take the opportunity to determine the WHY of your sheep enterprise.

Example:

- Takes the poorer country and makes a return, you all have poorer and frost-prone paddocks.

- Running sheep allows for rotation flexibility.

- Keep the focus on optimising profit rather than crop/ sheep ratios.

- Given the seasonal conditions, we might end up with more store-condition lambs at weaning.

- What is your marketing strategy?

- We are potentially in for an 18-24 month period of depressed prices and pressure on slaughter.

- The main opportunity still resides in pasture & feed management i.e. stocking rate.