“We’ll all be rooned,” said Hanrahan.

Turn on any media outlet feeding the anxiety over supply constraints, and it’s easy to understand why many are feeling distressed about the upcoming seeding season.

From a practical perspective, fear can motivate—but what we really need are cool, calm heads and clear strategies moving forward. Focus on controlling what you can, and the noise will remain just that—noise.

So, what do we know, and what can we do about it?

What Do We Know

Drilling Fertiliser

The vast majority of seeding fertiliser will be available for 2026—that is, compounds of some description.

You may not receive exactly what you ordered, but alternatives are being reworked. What we do expect are some delays in timing, primarily due to logistics, given the large volume being dispatched from in-shed stores while ships continue to arrive and manufacturing ramps up.

All companies fully recognise the on-farm impact and are doing everything possible to ensure seeding occurs on time. However, the need to source fertiliser from outside the Middle East may cause delays in a small portion of the total supply.

Action: Confirm product delivery dates and plan accordingly.

Nitrogen

Nitrogen has increased from approximately $1.90/unit four weeks ago to around $2.50–$3.00/unit, depending on source (with UAN currently significantly cheaper than urea).

Any uncontracted nitrogen will be priced at the current market rate and must be carefully assessed for return on investment.

While some UAN is manufactured locally, Western Australian production alone cannot meet seasonal demand. Therefore, imports will be required, and suppliers are likely only to procure fertiliser against firm grower commitments.

The expectation is that contracted seeding UAN supplies will be delivered, albeit under logistical limitations. Given recent events in China, some of the contracted UAN supply post sowing may come under pressure and as such, it is important to keep communication lines open.

Fuel

In regional Western Australia, most farmers purchase fuel through independent regional distributors rather than directly from major oil companies such as BP, Ampol, or Viva Energy.

Fuel supply to these distributors is largely governed by wholesale contracts with terminal owners. These contracts dictate source, volume access, and pricing. During supply constraints, major companies prioritise contractual obligations before supplying independents.

As demand has increased, rationing has occurred. Feedback from the Government roundtable indicates suppliers have maintained the mandated buffer (approximately 32 days of diesel), however delivery delays of 7–14 days have been experienced due to logistical limitations.

Recommendations from the roundtable included prioritising larger truck combinations to improve fuel flow to regional centres.

Expectation: Fuel supply should continue through March and April, though delays are likely due to logistics.

What Can We Do

1. Prioritise Logistics Management

2026 will be a year defined by logistics.

- Maintain calm, clear communication with suppliers

- Book early—flexibility will be limited

- Do not delay delivery slots—secure product on-farm

- Work closely with contractors, as they will also be under pressure

2. Manage UAN Supply Proactively

- Draw down UAN as early as possible

- Communicate refill requirements promptly

This supports both your own supply and the broader system by maintaining flow through manufacturing and logistics.

3. Maintain Fuel Reserves

Where possible, maintain fuel reserves through seeding and ideally through early post-emergent spraying and fertiliser spreading. Carefully consider the impact of pre-seeding preparations on total fuel reserves on-farm. Heavy burn processes, such as deep ripping, need careful analysis. Map the diesel requirements for seeding and post-emergent spray and fertiliser applications with a priority to cover these core processes.

While fuel is expensive, the cost of missing timely operations is significantly greater.

4. Phosphorus Strategy

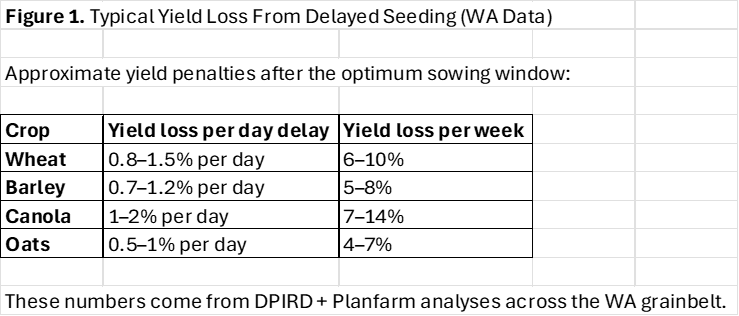

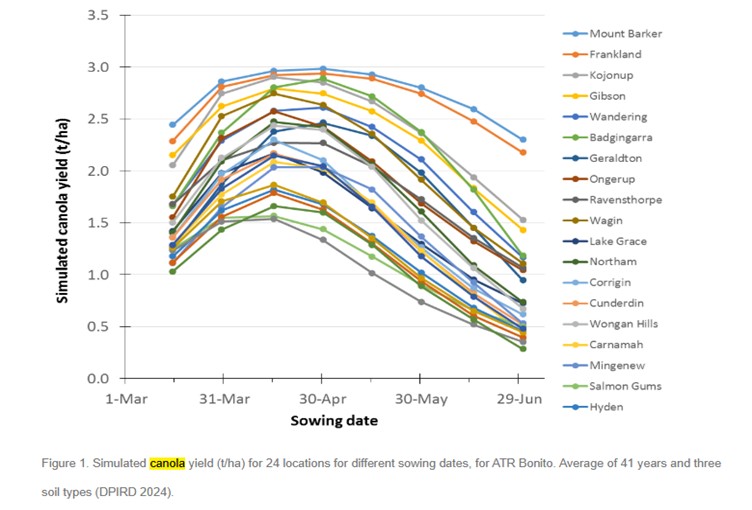

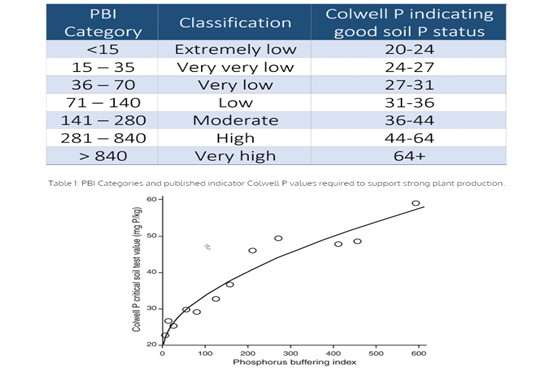

Seeding timing remains critical (see Figures 1 and 2).

If you need to stretch phosphorus until the next delivery or lack of total supply, consider the following rules of thumb:

a) Canola can operate at ~75% of cereal P due to better root exploration

b) If PBI is lower than Colwell P, P rates can be reduced (see Figure 3)

c) Wet soils require less P than dry soils

d) Warm, wet conditions increase mineralisation—allowing reduced P

e) P requirements after canola are typically 10–20% higher

f) Higher pH soils have greater P availability – watch sub 5 in CaCl

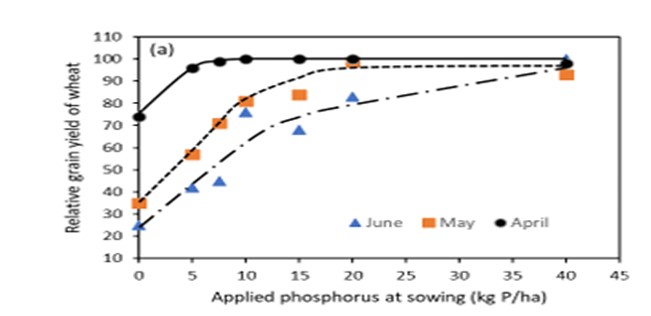

g) The first 8–10 units of P deliver the greatest yield response; marginal returns decline thereafter (see Figure 4)

h) Subsoil constraints reduce root access—may require higher P

i) Wheat is most responsive to P; oats are least—reduce oats before wheat

j) Only ~15% of applied P is used in year one; the remainder contributes to legacy P

Key point: Avoid removing P entirely; small applications still deliver strong yield benefits.

Figure 1. Impact of Seeding Delay

Figure 2. Canola Yield Impact from Sowing Time

Figure 3. PBI and Colwell P Guide

Figure 4. P Marginal Response Curve x P and Rainfall (Seeding Time)

(Note: this is an example only – individual soil types and location will have different P response curves)

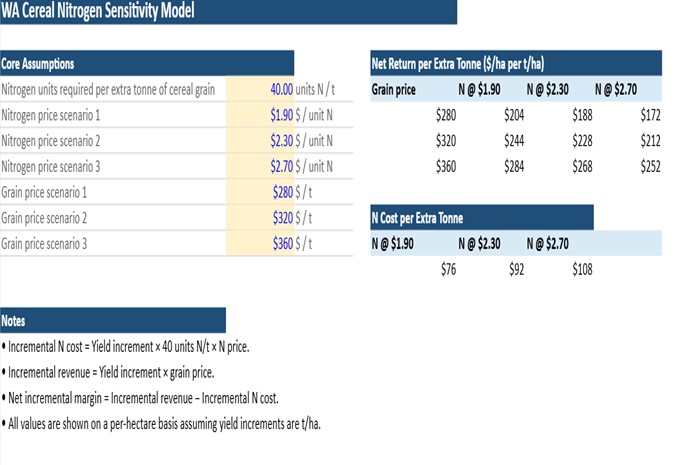

5. Nitrogen Strategy

Nitrogen is the true variable cost. Whether you target a 1t crop or a 5t crop, you still need to spray, seed, fertilise and harvest. The final level of nitrogen is truly variable in nature given the season you receive. Be careful not to drop a key profit-influencing nutrient without careful consideration (see Figure 5). Take the time to assess each paddock for tailored nitrogen requirements rather than broad-brush approaches. Nitrogen may need to be rationed, and as such, careful considerations on ROI should be assessed.

Key considerations:

a) High biomass from 2025 means N tie-up is likely to lead to reduced efficiency.

– In extreme cases, strategic stubble reduction may be considered.

b) Nitrogen applied after Z31 in cereals typically influences protein, not yield.

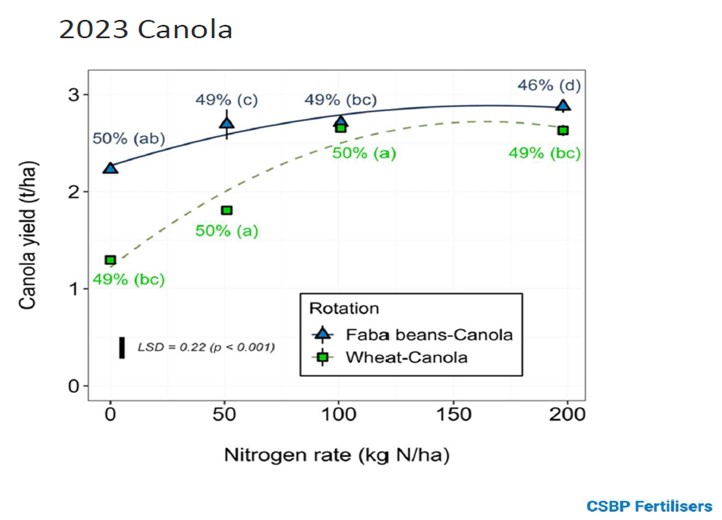

c) Canola uses ~80 units N/t but only exports ~50%

→ Following crops benefit from residual N

d) Organic carbon is a strong indicator of mineralisation potential (OC% x GSR x 0.15 = Estimated Soil N).

e) February rainfall may increase mineralisation for those fortunate to receive it -consider soil testing

f) Leverage N from legumes (including multi-year carryover effects).

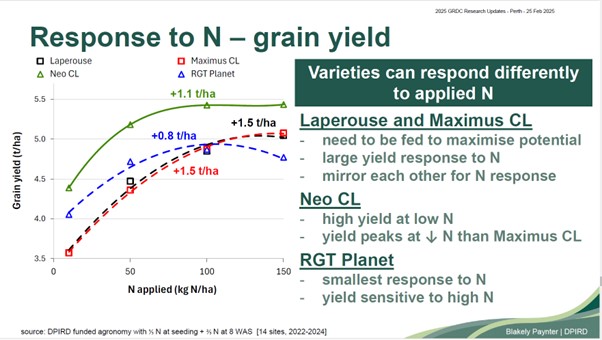

g) Crop type matters-varieties differ in N efficiency (see Figure 6).

h) Hybrid canola is highly responsive to nitrogen-avoid under-fertilising (see Figure 7).

Figure 5. Nitrogen Sensitivity

Figure 6. Varietal Response to Nitrogen

Figure 7 Nitrogen Response Curve

6. Grain Marketing

Grain marketing opportunities are emerging due to global supply disruptions.

While input costs have risen, grain prices have also strengthened from a low base.

Stay proactive:

Engage regularly with marketers

Capture price opportunities where appropriate

It would be a missed opportunity to absorb the downside of the crisis without capturing the upside.

Wrapping Up

While this situation presents a significant challenge, it also creates an opportunity for those willing to adapt.

Opportunities include:

a) Reassessing input strategies and identifying where high-cost inputs deliver strong ROI

b) Building more resilient systems (fuel storage, fertiliser capacity)

c) Capturing improved grain prices

d) Rethinking rotations and biological nitrogen strategies

Final Thought

The coming months will be challenging.

Gather your advisory team, communicate clearly and frequently, make calm and considered decisions—and most importantly, look for the opportunities that will exist for those prepared to find them.